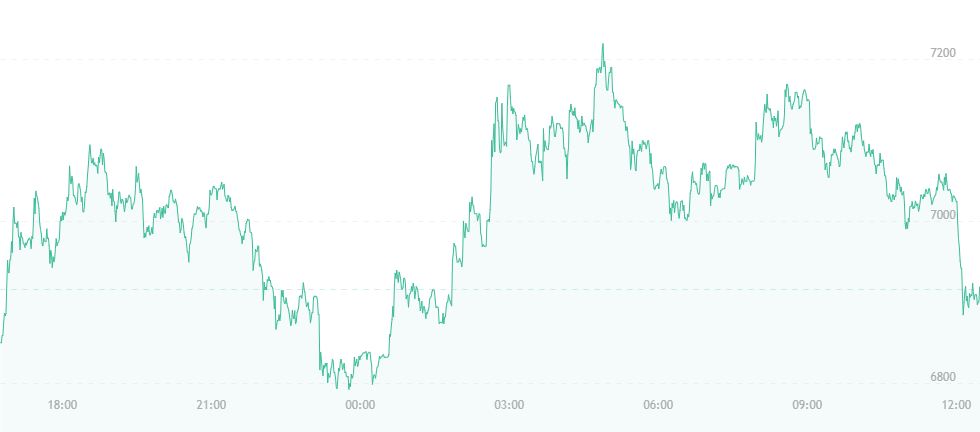

Bitcoin’s price has incurred a small jump. After yesterday’s trading lows of $6,600 – $6,900, the current mark for bitcoin’s price is just under $7,100 – a small, but noticeable step forward after what can be labeled a very tumultuous week.

For the most part, however, cryptocurrencies remain in the red, with major bitcoin competitors like ether trading at just under $400 and litecoin sitting at about $116. Other currencies, like Ripple’s XRP and bitcoin cash, are down approximately 20 to 30 percent from last week’s figures. Overall, the market has lost a total of nearly $114 billion, though today marks a seven percent increase from March 30.

The primary sentiment was that Hong Kong-based exchange OKEX and the liquidation of its futures contracts may have led to the sudden drop. All futures trading has since resumed on the platform, though many contracts ultimately disappeared or traded for significantly smaller figures. Executives claim the move was part of a plan to prevent irregular sell-offs in the future, while others claim the exchange was legitimately trying to manipulate the bitcoin price.

In addition, several regulatory fears continue to emerge from Japan, a global bitcoin hub. Recently, two separate exchanges have taken back their applications with the Financial Services Agency (FSA), citing they were not interested in being monitored by financial and/or government authorities.

To an extent, this can be understood. The decentralized nature of cryptocurrencies would undoubtedly be compromised by consistent regulation, and the crypto-environment as we know it would probably take a tumble or change drastically.

However, one idea behind a recent string of banks working to prevent customers from purchasing digital currencies is that traditional financial institutions feel they cannot compete with the non-regulated atmosphere of crypto, and thus are working not necessarily to protect customers or their funds, but rather to stay relevant. If all finances became completely unregulated and there was no longer a need for government or authoritative eyes to examine financial dealings, modern-day banks would probably lose their footing.

Are banks primarily worried about their own futures? That’s certainly a question worth exploring.

The latest bank to take a hard stance against cryptocurrency is the National Bank of Kazakhstan. The organization’s chairman released a statement on Friday that the country is examining a full ban of every digital currency available in today’s market. State departments are concerned about the country’s national currency, the tenge, and whether it could lose stability if customers regularly choose to trade it in for crypto. Granted residents decide the power lies in digital currencies, the tenge could potentially become obsolete, which may lead to economic problems like inflation.

The chairman also explains that he’s concerned about illicit activities cryptocurrencies can allegedly birth – issues like tax evasion and money laundering. This is a common argument, especially among government figures or those seeking to bar cryptocurrency permanently.

At the end of the tunnel, however, is a faint light, as most analysts suggest the recent crypto-crash may finally be reaching its end, and a strong period of recovery is on the way. They suggest things could start as early as April during tax season, while also claiming that futures trading is likely to increase as well, thus pushing the price even further.