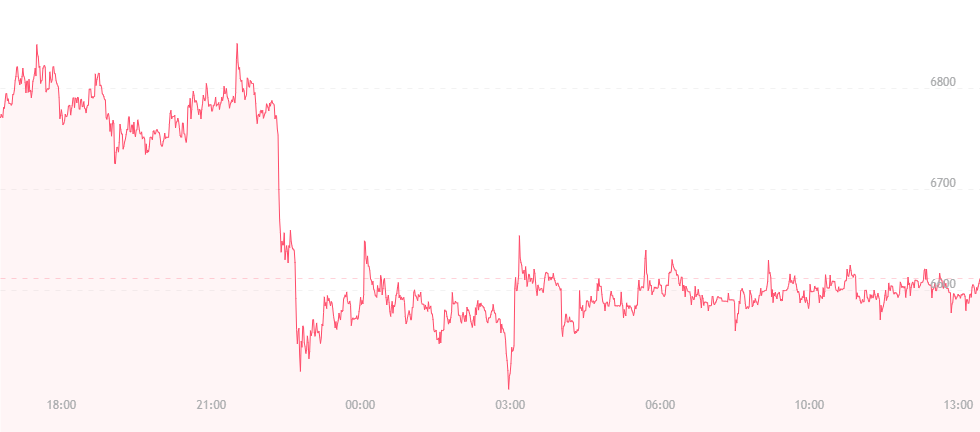

Bitcoin is down another $100. After yesterday’s “high” of roughly $6,700, the currency has dropped down to $6,600. This appears to be an ongoing theme with bitcoin as of late; the currency has been falling by approximately $100 per day since the week began.

Though the price is repeatedly falling, this could suggest that bearish trends are not as powerful as when bitcoin first fell from the $9,000 or even $8,000 range. Additionally, resistance levels could allegedly be strengthening as the technology behind bitcoin incurs further implementation and popularity – especially in the business world.

Indeed, however, the cryptocurrency scene has been marred by several massive decisions over the past few days. In review, we’ve examined that Coincheck may be “rescued” by Monex Group in Tokyo, the second time since Kraken took over Mt. Gox accounts that a victimized Japanese exchange has been “given a backup system.”

Though the price quickly rose to roughly $7,500 following the news, things swiftly took a turn for the worse. The hack on Verge and the cancellation of bitcoin allowances in India – a country that accounts for nearly 10 percent of global bitcoin transactions – certainly imposed repercussions on the digital currency, which may have brought the price down to its current level.

However, it appears a light is glowing at the end of what was looking like a long, dismal and particularly dark tunnel. South Korea – which accounts for nearly 25 percent of the globe’s crypto transactions – is renewing its love for bitcoin following hefty and daring moves towards regulation.

The environment in Korea has been somewhat up-and-down since January, with many sources originally (and falsely) reporting at one time that the country was on the brink of banning crypto exchanges permanently. Though this news was scrapped and the true stories behind upcoming regulation were brought to light, the price of bitcoin took a near-10 percent stumble, and things have gone relatively downhill since then.

To an extent, South Korea is still home to many contradictions surrounding the cryptocurrency arena. The nation’s biggest bank Kookmin, for example, has officially sworn off providing financial services to platforms that deal or trade in digital assets.

This seemed like a nasty blow to a once enthusiastic community, but that move was countered by financial establishments like Shinhan and Woori – two of South Korea’s largest commercial banks. Both institutions have continued to support cryptocurrency platforms, and have backed a growing number of blockchain and bitcoin enterprises since January, ranging from cold wallet storage to the utilization of the Ripple Network.

In addition, Shinhan is now partnering with Ethereum-based banking platform OmiseGo to potentially enhance the blockchain presence in Asia.

CEO Jun Hasegawa released the following statement:

“The OMG platform, using the Plasma architecture, is being built as a public network that is powered by Ethereum. The first phase of the wallet SDK was recently released, and is available for anyone to use. We want to make it easy for those who need an online asset exchange as part of their business to connect seamlessly to the OMG network.”

Financial trends in Asia – particularly in China, Japan and South Korea – have a way of catching on in neighboring countries. If we’re to assume that banks are becoming more open and friendly towards cryptocurrency ventures, it won’t be long before that attitude spreads, which may potentially lead to the recovery bitcoin so rightfully deserves.